uca Bregoli, co-founder and COO of co-living operator Cove, wants to scale up the business and expand the firm’s presence in the Asia Pacific region.

A few months ago, Cove launched Cove Luxe, a new line of co-living spaces with more upscale in-room amenities, furnishings and services.

Its latest offering is the Cove Luxe across four conservation shophouses at 31, 33, 35 and 37 Kinta Road in the Farrer Park neighbourhood. Renovations were completed in June and the property was opened shortly after.

The Cove Luxe at Kinta Road has 26 en suite rooms and shared spaces and is already 92% occupied. According to the Cove website, the room rates at Cove Luxe on Kinta Road range from $2,250 per month for a 129 sq ft, en suite master bedroom on the ground floor, to $3,600 a month for a 312 sq ft, en suite studio on the second floor.

In Little India, Cove and its partner, construction and development company Eco-Energy, won the Singapore Land Authority (SLA) tender to repurpose the row of two-storey heritage shophouse-style buildings at 79 to 95 Hindoo Road for co-living. It was the first time that SLA had offered shophouse-style state buildings for tender as co-living concepts that offer community bonding activities and green initiatives. The tender drew 16 bids, according to SLA in a media release on Aug 23.

Renovations are underway to repurpose the heritage property at Hindoo Road, which is targeted to open in 1Q2024 as “1925 Quarters” by Cove. The property will have 18 apartment units across a gross floor area of 1,700 sq m (18,299 sq ft).

With the launch of Cove Luxe, the co-living operator now has three different tiers of products. The top-tier Cove Luxe has rates starting from $2,650 per month, offering a fully furnished luxury room and a comprehensive kitchen. The mid-tier Cove Classics has fully furnished rooms and kitchens, with monthly room rates from $1,600. Cove Basics, as the name suggests, offers basic furnished rooms and a shared kitchen, with room rates from $1,300 a month.

Cove will continue to offer a wide range of co-living spaces. “A platform like ours needs to have a variety of housing options for people to choose from — whether it’s a single apartment in a city location, a studio in a conservation shophouse, or a house in a residential estate,” says Bregoli.

Regional expansion

Since Cove was founded in 2018, it has grown its co-living platform to 1,000 rooms in Singapore and about 4,000 rooms in Indonesia, spread across Jakarta, Bandung and Bali. Keppel Land took a minority strategic stake in Cove as the lead investor in the co-living operator’s US$4.6 million Series-A funding round in December 2020.

In addition to its partnerships with Keppel Land and Lippo Group in Indonesia, Cove has struck up partnerships with asset owners in Singapore, such as 8M Real Estate and Meir Collective.

Cove’s properties have an average occupancy rate of 95% in Singapore and 88% in Indonesia. The co-living operator has an annual recurring revenue of $38 million, says Bregoli. However, the first nine months of 2023 saw a 100% growth in net revenue, he says.

Corporates have been a good source of recurring revenue, adds Bregoli. Cove works directly with corporates to house their expatriate staff working in Singapore and Indonesia; soon, it will do this in South Korea as well. On Sept 25, Cove signed a memorandum of understanding with South Korean real estate asset manager Honors Asset Management. The exclusive partnership will allow Cove to enter and operate in the South Korean market.

Singapore — a critical market

Bregoli is also in discussions with several other asset managers and investors to expand Cove’s presence in Asia Pacific. While Bregoli is keen to expand Cove’s regional footprint, Singapore remains a critical market for the firm. He believes there are still opportunities to grow and strengthen the firm’s product offerings.

For instance, he hopes to open a hotel concept in Singapore. “The hospitality market in Singapore is very competitive, but we have a very specific hotel concept in mind, and we’re looking out for the right property to launch it,” says Bregoli.

Over the past few years, more institutional investors and real estate investment firms have added co-living properties to their portfolios, he says.

“The concept of co-living in Singapore is much more accepted among landlords and investors today,” says Bregoli. “In the budding days about six years ago, it was almost taboo to propose the concept of co-living to asset owners.”

Co-living operators are also maturing, adds Bregoli, with most of them scaling up their operations, increasing their professionalism in service delivery, and adapting to changes in consumer demand.

Scarcity of properties

According to a JLL report on the co-living sector in June, the biggest hurdle for co-living operators is the scarcity of properties.

The government is responding to calls for more co-living spaces from operators and tenants. Following the success of the tender for the property at Hindoo Road, SLA launched a second state property for tender on Aug 16. The property is 26 Evans Road, within walking distance of the Singapore Botanic Gardens and just off Bukit Timah Road. The property has 6,555.5 sq m (70,563 sq ft) of gross floor area, and is to be repurposed for co-living.

Co-living properties in Singapore are typically properties zoned for residential or hospitality use. Co-living spaces in properties zoned for residential use must have a minimum lease of three months. There is also a cap of six unrelated persons residing in one private residence, and this also applies to a tenant who sublets the property. “I think the regulations can be reviewed to take into account the asset type and the floor area of living spaces in each property,” says Bregoli.

There is greater flexibility for properties zoned for hospitality use as those licensed as serviced apartments have a minimum stay of seven days, while those with hotel licences can be rented out daily.

Biggest players

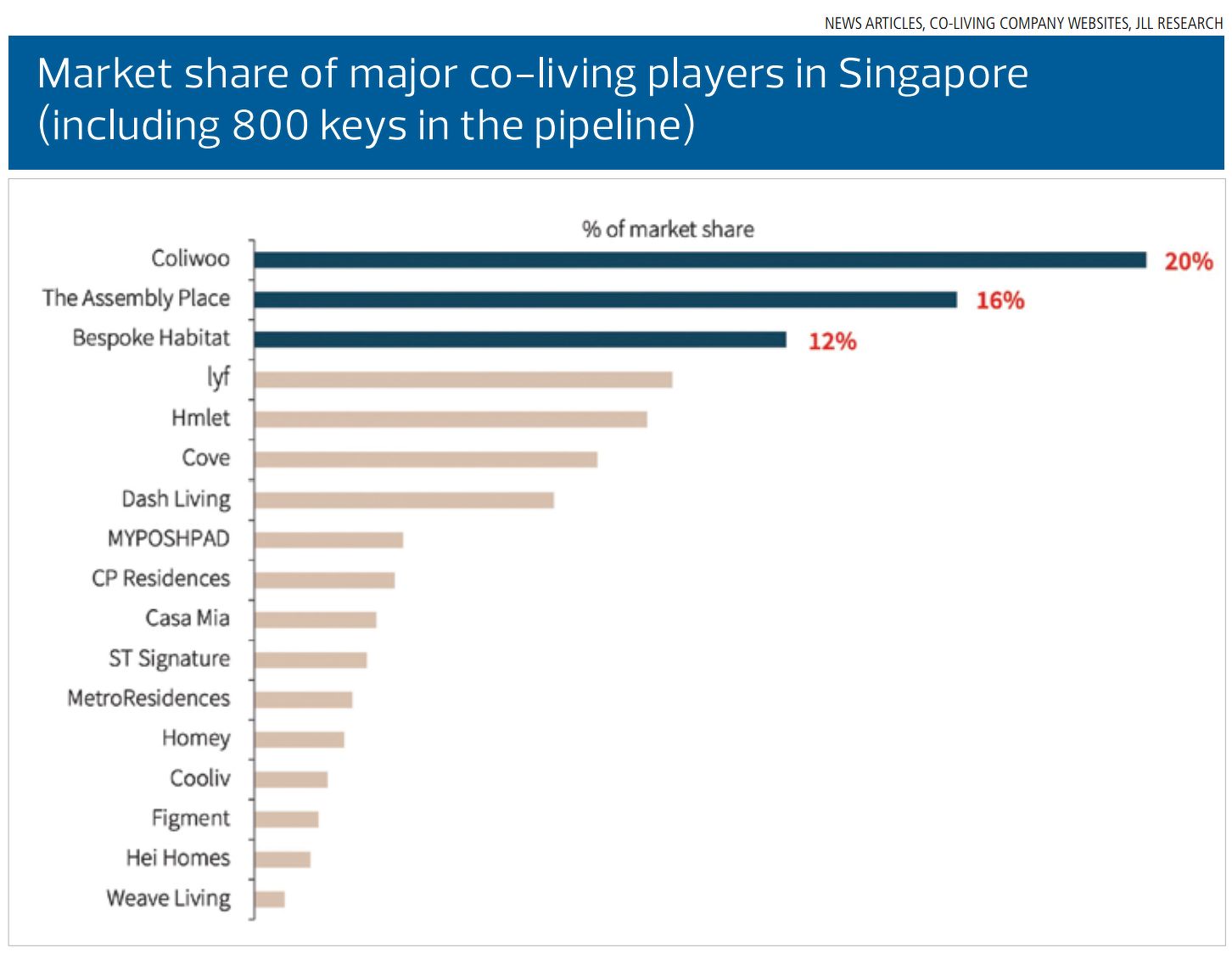

The co-living market in Singapore has consolidated to about half a dozen established and well-funded players. The three biggest players by market share, according to the JLL report, are Coliwoo (20%), followed by The Assembly Place (16%) and Bespoke Habitat (12%). Cove is ranked sixth, after Lyf and Hmlet (rebranded Habyt), with Dash Living in seventh place.

Bregoli takes these rankings with a pinch of salt, commenting that the figures do not reflect the individual operators’ business health or the strength of their co-living products.

It has become clear that the well-funded co-living players with financial backing from institutional investors or venture capital funds are better positioned to scale up, improve their product offerings and grow their member base.

“For Cove, we are in a good position in both Singapore and Indonesia, plus, we have a strong line-up of business-to-business contracts that will support our occupancy rates for the long term,” says Bregoli.