B2B edtech firm Eupheus Learning is among a handful of edtech startups that managed to grow exponentially with sound economics. The company grew 4X in its last two fiscal years: rising to Rs 99 crore in FY23 from Rs 23 crore in FY21.

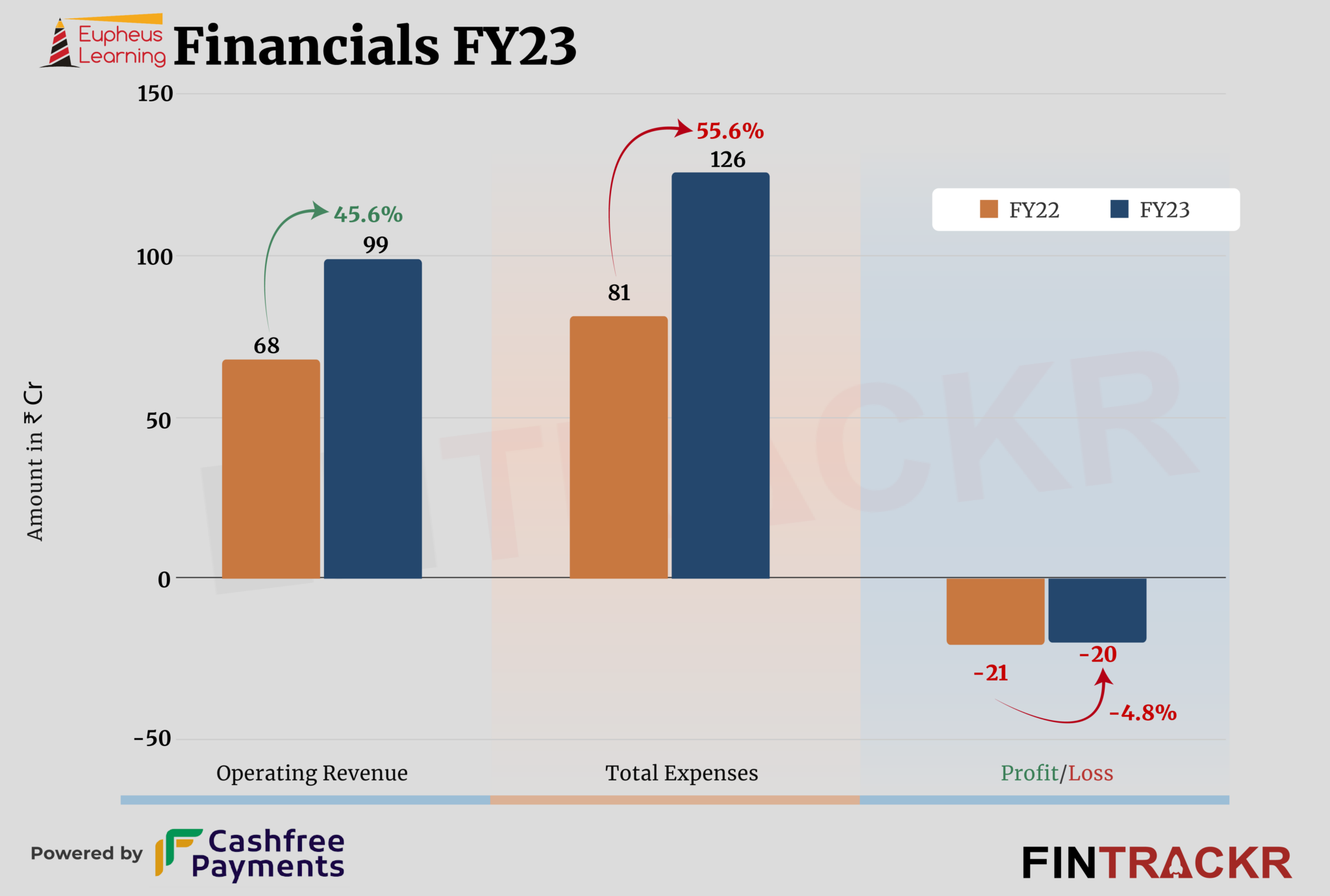

When it comes to YoY growth, Eupheus Learning’s revenue from operations increased 45.6% to Rs 99 crore in FY23 from Rs 68 crore in FY22, its consolidated financial statements filed with the Registrar of Companies show.

Eupheus Learning provides digital curriculum along with supplemental modules to schools (books). The sale of printed books accounted for 95% of the total operating revenue which increased 94.9% to Rs 94 crore in the fiscal year ending March 2023.

In 2021, the company also acquired ClassKlap which enables schools to manage their operations including administrative and academic. The rest of the revenue came from the sale of digital products.

Moving over to the cost side, the procurement of modules accounted for 28.5% of the overall expenditure. This cost increased by 28.6% to Rs 36 crore in the last fiscal year.

Its employee benefits, finance, advertising, legal-professional, traveling, and other overheads took its total cost to Rs 126 crore in FY23 from Rs 81 crore in FY22. Head to TheKredible for the detailed expense breakup.

Despite decent growth in scale, Eupheus Learning reduced its losses marginally which stood at Rs 20 crore in FY23. Its ROCE and EBITDA margin improved to -14% and -10.6%, respectively. On a unit level, the company spent Rs 1.27 to earn a rupee in the last fiscal year.

Eupheus Learning last raised $10 million in its Series C round led by private equity platform Lightrock India in September 2021. According to startup data intelligence platform TheKredible, Sixth Sense India is the largest stakeholder with 31.82% followed by Lightrock which commands 16.18% of the company.

While the improving financials will help, it remains unclear if the firm has done enough to raise a fresh round at the same or higher valuation of 2021. Simply moving to a lower burn rate will not help Eupheus, especially in the hyper competitive market it operates in. Scaling up will always come at a cost, as selling expenses are high for the category. While its numbers prove that it has a product which has a market, the road to sustainable numbers still looks long.